Summary

A Python project that simulates credit scoring based on behavioral metrics and stores the results in a MySQL database. It uses a simplified version of the FICO scoring model, applying weighted factors like payment history, credit utilization, and account age. Final scores are scaled to the industry-standard 300–850 range.

Workflow

- Simulate user financial data using Python

- Calculate weighted credit factors based on real-world behavior

- Generate scaled credit scores between 300–850

- Auto-check and create database columns if missing

- Insert processed results into a MySQL database

Tech Stack

- Python – Core logic and data transformation

- Pandas – Data wrangling and metric calculations

- MySQL – Backend storage

- MySQL Connector – Python-SQL integration

- Git & GitHub – Version control and hosting

1. Input Dummy Data in Python

2. Calculation of credit score

This project calculates synthetic credit scores using Python and stores them in a MySQL database. The score is based on a simplified version of the FICO model, which is the industry standard used by lenders to evaluate credit risk.

The formula used is:

raw_score =

(payment_history * 0.35) +

(credit_utilization * 0.30) +

(credit_history_length * 0.15) +

(credit_mix * 0.10) +

(new_credit * 0.10)

Each component is computed from user-like input data and reflects real-world credit behavior:

Payment History (35%)

What it reflects: Whether the user has a history of paying on time.

How it’s calculated:

payment_history = (on_time_payments / total_payments) * 100If a user made 28 payments on time out of 30, the score is 93.3%.

Credit Utilization (30%)

What it reflects: How much of the user’s available credit is being used. Lower is better.

How it’s calculated:

credit_utilization= (credit_used / credit_limit) * 100

credit_utilization_score = 100 - credit_utilization

If someone is using 30% of their limit, they get 70% in this category.

Length of Credit History (15%)

What it reflects: How long the user has had credit.

How it’s calculated:

credit_history_length = (oldest_account_years / 10) * 100The scale is capped at 10 years for simplicity. Someone with 5 years gets 50%.

Credit Mix (10%)

What it reflects: Whether the user has different types of credit (e.g. credit cards, loans, mortgages).

How it’s calculated:

types = has_credit_card + has_loan + has_mortgage

credit_mix_score = {0: 0, 1: 50, 2: 75, 3: 100}[types]The more diverse the mix, the higher the score.

New Credit (10%)

What it reflects: Whether the user has recently opened new accounts or applied for credit.

How it’s calculated:

new_credit = max(0, 100 - (num_inquiries * 15))Each inquiry reduces the score by 15 points. Maxed at 6+ inquiries = 0%.

Scaling

After summing all weighted components, the raw score (out of 100) is scaled to match the FICO-like range of 300–850:

credit_score = 300 + (raw_score / 100) * 550This scoring system is ideal for simulation, education, or as the backend for a credit modeling web app. While simplified, it mirrors the logic of real credit algorithms in a transparent and customizable way.

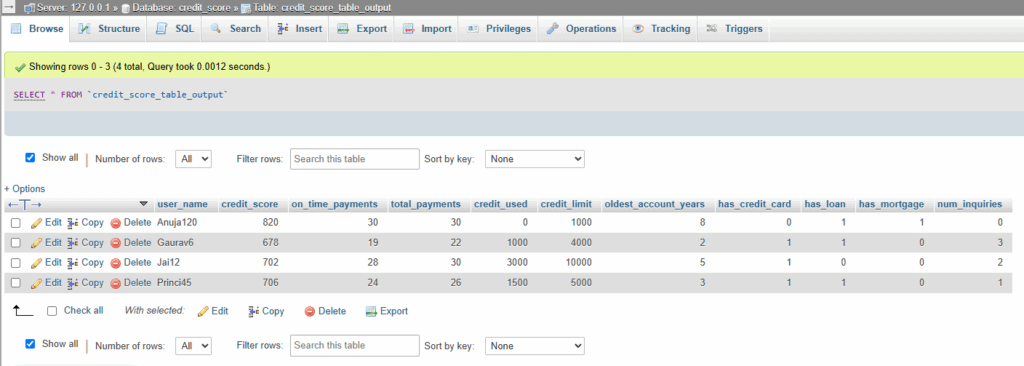

3. Output

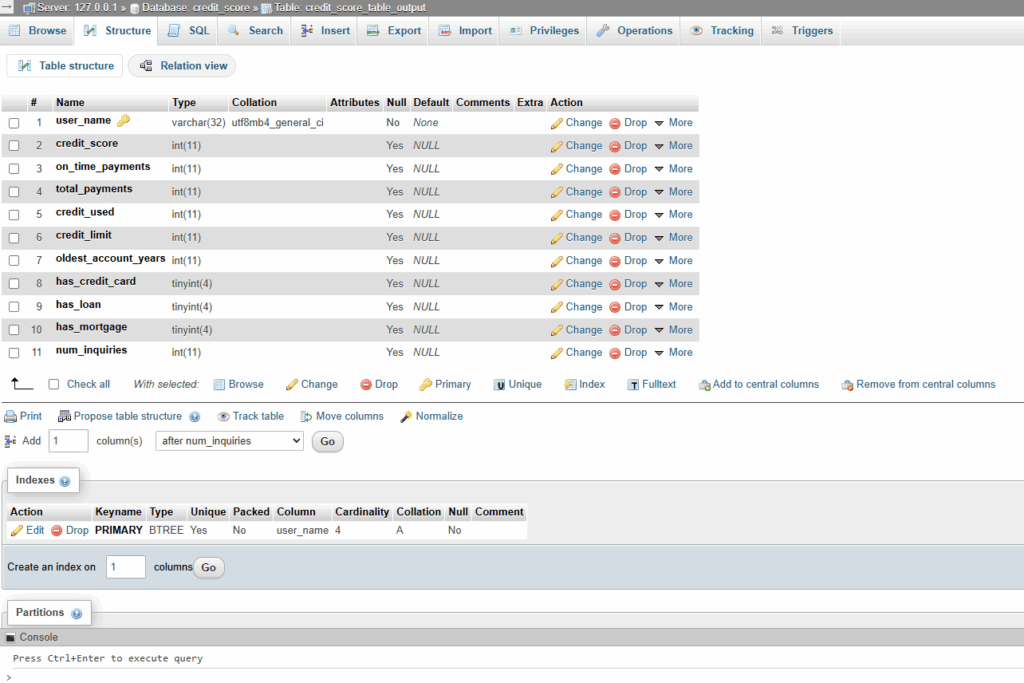

Database structure in MySQL

Output Data calculating credit score in MySQL